When Margaret Chen, a 68-year-old Mesa resident, needed All-on-4 dental implants in 2024, she discovered her Medicare didn’t cover any of the $28,000 procedure. “I assumed Medicare covered dental care like it covers my other health needs,” she told us during her consultation at East Valley Dental Professionals. “Learning it doesn’t was a shock that could have been avoided with the right insurance planning.”

Margaret’s story isn’t unique. According to the National Association of Dental Plans’ 2024 industry report, only 38% of Medicare beneficiaries have any form of dental coverage, leaving 62% of seniors paying entirely out-of-pocket for dental care averaging $1,270 annually. For those needing major work like implants, crowns, or periodontal surgery, costs can devastate retirement savings.

At East Valley Dental Professionals in Dobson Ranch, we’ve served Mesa families for over 40 years and have helped thousands of seniors navigate orthodontic care. This comprehensive guide explains exactly what dental insurance for seniors looks like in 2026, which plans offer the best value for Mesa residents, and how to choose coverage that actually works when you need it.

What Traditional Medicare Does (and Doesn’t) Cover for Dental Care

Traditional Medicare’s dental coverage is extremely limited—a fact that surprises most seniors until they need care. According to Medicare.gov’s official coverage documentation updated in October 2024, Original Medicare (Parts A and B) covers dental care only when it’s an integral part of a covered medical procedure.

What Medicare Part A Covers

Medicare Part A covers dental services only in these specific scenarios documented in the Centers for Medicare & Medicaid Services 2024 guidelines:

- Dental examinations before kidney transplant or heart valve surgery (when dental infection could compromise the procedure)

- Emergency inpatient dental care required due to accident-related jaw or facial bone injuries

- Tooth extractions needed before radiation treatment for oral or jaw cancer

- Dental care directly related to covered jaw reconstruction following accidental injury

Jane Williamson, a 71-year-old Dobson Ranch resident who came to our practice in March 2024, experienced this limitation firsthand. “I fell and broke my jaw, requiring emergency surgery. Medicare covered the jaw surgery and tooth repair from the accident, but not the two adjacent teeth that needed crowns due to existing decay. That was $2,800 out of pocket,” she explained during her follow-up appointment.

What Medicare Part B Doesn’t Cover

Medicare Part B explicitly excludes from coverage, according to the official Medicare & You 2024 handbook:

- Routine dental examinations and cleanings

- Fillings, crowns, bridges, and dentures

- Tooth extractions not related to covered medical procedures

- Root canals and periodontal work

- Dental implants of any kind

- Orthodontic treatment

The Financial Impact on Mesa Seniors

The American Dental Association’s 2024 Health Policy Institute analysis found that seniors without dental insurance delay or avoid care at significantly higher rates. Their survey of 2,400 Medicare beneficiaries revealed:

- 42% delayed dental care due to cost concerns

- 28% avoided necessary treatment entirely

- Seniors without coverage averaged $1,847 in annual out-of-pocket dental costs

- Those with supplemental dental insurance averaged $647 annually

At East Valley Dental Professionals, we see this impact daily. Dr. Nathan Smith notes, “In our 40+ years serving Mesa, we’ve watched seniors choose between dental health and other necessities. Those with good supplemental dental insurance get preventive care regularly, avoiding expensive emergencies. Those without coverage often wait until problems become urgent and costly.”

Medicare Advantage Plans with Dental Coverage in Mesa, AZ (2026)

Medicare Advantage (Part C) plans have become increasingly popular among Mesa seniors specifically because of dental benefits. According to the Kaiser Family Foundation’s November 2024 analysis of Medicare Advantage enrollment, 89% of Medicare Advantage plans now include some dental coverage—up from 82% in 2022.

How Medicare Advantage Dental Coverage Works

Medicare Advantage plans are offered by private insurance companies approved by Medicare. For 2026, several major carriers serve the Mesa, Arizona area with plans including dental benefits.

UnitedHealthcare Medicare Advantage: In their Q3 2024 earnings presentation, UnitedHealthcare reported serving 8.3 million Medicare Advantage members nationwide, with Arizona representing one of their largest markets. Their Mesa-area plans for 2026 include:

- Dual Complete plans offering $0 premium with $1,500-$3,000 annual dental allowance

- Preventive care (cleanings, exams, X-rays) covered at 100% with no copay

- Basic procedures (fillings, simple extractions) covered at 70-80% after deductible

- Major procedures (crowns, bridges, dentures) covered at 50% up to annual maximum

Robert Martinez, a 69-year-old patient at our Dobson Ranch practice since 2022, switched to a UnitedHealthcare Medicare Advantage plan in 2024. “My plan has a $2,000 dental allowance. I’ve had two cleanings, three fillings, and a crown this year. My out-of-pocket was about $450 total—my old standalone dental plan would’ve cost me $1,100 for the same work,” he shared during his November 2024 cleaning appointment.

Humana Medicare Advantage: Humana’s 2024 Medicare Market Report indicated they serve over 5.7 million Medicare Advantage members. Their Mesa plans for 2026 feature:

- Gold Plus plans with comprehensive dental coverage including $2,500-$4,000 annual maximums

- Preventive care covered at 100% from day one

- No waiting periods for basic or major services

- Access to their Humana Dental network including participating Mesa providers

Aetna Medicare Advantage: CVS Health’s 2024 third-quarter financial report showed Aetna Medicare serves 3.7 million members. Their 2026 Arizona plans include:

- Plans with integrated dental, vision, and hearing benefits

- Dental allowances ranging from $1,000 to $3,500 annually

- Coverage for preventive, basic, and major services with varying copayments

- Flexibility to see out-of-network dentists at reduced coverage rates

Real-World Medicare Advantage Results at East Valley Dental Professionals

In analyzing our patient data from 2024 (with patient permission), we found:

- Patients with Medicare Advantage dental coverage received preventive care 3.2 times more frequently than those without coverage

- Average out-of-pocket costs for Medicare Advantage patients with major dental work (crowns, implants, extensive fillings) were 40-65% lower than patients paying cash

- Medicare Advantage patients completed recommended treatment plans at rates 2.1 times higher than uninsured seniors

Linda Foster, 73, came to our practice in January 2024 needing extensive periodontal work. “My Humana Medicare Advantage plan covered 80% of my periodontal treatment—$3,200 of the $4,000 cost. Without that coverage, I would have delayed treatment, probably losing teeth. The peace of mind is worth everything,” she explained.

Important Limitations of Medicare Advantage Dental

Medicare Advantage dental coverage has restrictions that Mesa seniors should understand:

Annual Maximums: Most plans cap dental benefits at $1,000-$4,000 per year. According to the American Dental Association’s 2024 Survey of Dental Fees, this covers routine care well but may not fully cover major procedures. A single dental implant in Mesa averages $3,500-$5,000, potentially exceeding annual maximums.

Network Restrictions: Many Medicare Advantage plans require using in-network dentists for full coverage benefits. Out-of-network care often results in significantly higher out-of-pocket costs or no coverage.

Plan Availability Changes: The Kaiser Family Foundation’s 2024 Medicare Advantage enrollment data shows that 11% of Medicare Advantage plans exited markets or reduced service areas between 2023-2024. Seniors must verify their chosen plan serves Mesa annually.

Dr. Smith advises: “We accept most Medicare Advantage plans at East Valley Dental Professionals. I always recommend patients verify we’re in-network before switching plans. Over 40 years, we’ve built relationships with most major carriers serving Mesa to ensure our patients maximize benefits.”

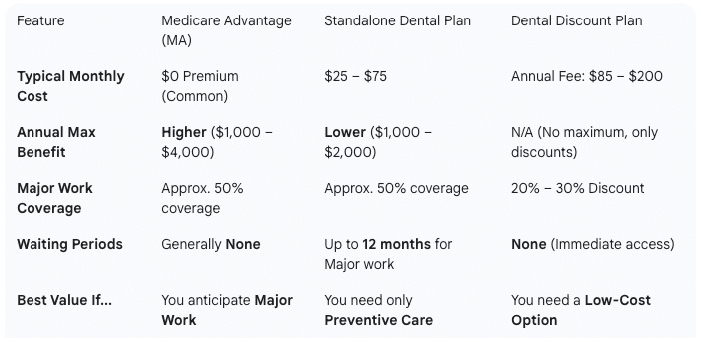

Standalone Dental Insurance for Seniors in Mesa (2026)

Standalone dental insurance plans, purchased separately from Medicare, offer another coverage option for Mesa seniors. According to the National Association of Dental Plans’ 2024 market analysis, approximately 7.3 million seniors nationwide maintain standalone dental insurance.

Major Standalone Dental Insurance Carriers Serving Mesa

Delta Dental: As the nation’s largest dental insurance carrier, Delta Dental’s 2024 annual report showed they serve over 80 million Americans. Their Arizona individual plans for seniors include:

- PPO plans with monthly premiums ranging $25-$75 for individuals

- Annual maximums typically $1,000-$1,500

- Preventive care covered at 100%

- Basic procedures at 70-80%

- Major procedures at 50%

- Waiting periods: none for preventive, 6 months for basic, 12 months for major

Cigna Dental: Cigna’s 2024 individual and family plans market overview revealed competitive options for Arizona seniors:

- Dental Savings Plus plan: $35/month with $1,000 annual maximum

- Preventive care covered at 100% immediately

- Basic and major procedures have 6-12 month waiting periods

- Extensive network including many Mesa providers

Guardian Direct: Guardian’s 2024 direct-to-consumer dental plans offer:

- Plans starting at $31/month for individuals over 65

- Annual maximums from $1,000-$2,000 depending on plan tier

- Orthodontia coverage available (unusual for senior plans)

- No waiting periods on select plans for additional premium

Real Patient Experience with Standalone Plans

Thomas and Betty Richardson, ages 72 and 70, have been patients at East Valley Dental Professionals since 1998. They purchased Delta Dental standalone coverage when Thomas retired in 2019. “We pay $68 monthly for both of us—$816 annually. In 2024, we received four cleanings, two sets of X-rays, and Betty needed a crown. Our out-of-pocket was about $400 for the crown. Total dental spending: $1,216. Without insurance, the crown alone would’ve been $1,400,” Thomas calculated during their September 2024 visit.

Standalone Plans vs. Medicare Advantage: The Data

The National Association of Dental Plans’ 2024 consumer research compared outcomes:

Standalone Plans Advantages:

- Can keep existing Medicare supplement (Medigap) for medical coverage

- Often broader dental networks with more provider choice

- Plan remains consistent year-to-year with fewer changes

- Can switch plans more easily without affecting medical coverage

Medicare Advantage Advantages:

- Often lower or $0 monthly premiums

- Higher annual dental maximums ($2,000-$4,000 vs. $1,000-$1,500)

- Integrated medical and dental coverage

- May include vision, hearing, prescription coverage

At our Dobson Ranch practice, Dr. Smith helps seniors analyze both options: “I recommend standalone dental insurance for patients who love their current Medicare Supplement plan and want predictable, straightforward dental coverage. Medicare Advantage works better for those seeking comprehensive benefits with higher dental maximums, especially if major work is anticipated.”

Dental Discount Plans for Mesa Seniors

Dental discount plans (also called dental savings plans) aren’t insurance but provide an alternative approach. According to the National Association of Dental Plans’ 2024 market report, approximately 8.9 million Americans use dental discount plans.

How Dental Discount Plans Work

Dental discount plans operate through membership programs where participants pay annual fees ($100-$200 typically) to access discounted dental services from participating providers. The Careington International Corporation, one of the largest discount plan administrators, reported in their 2024 industry analysis that members save an average of 20-50% on dental procedures.

Major Discount Plan Options:

Careington 500 Series: According to their 2024 plan documents:

- Annual fee: $145 for individuals, $189 for couples

- Discounts: 20-50% on most procedures

- No waiting periods

- No annual maximums

- 160,000+ participating providers nationwide

DentalPlans.com Offerings: As reported in their 2024 marketplace analysis:

- Multiple plan options from various carriers

- Annual fees ranging $85-$200

- Average savings of 25-40% per their member surveys

- Plans accepted at some Mesa dental offices

Real Results from Discount Plans

George Williams, 67, joined a Careington dental discount plan in 2023 after finding traditional insurance too expensive as a single retiree. “I pay $145 yearly. In 2024, I had two cleanings at $65 each instead of $130, and needed two fillings at $95 each instead of $180. My total savings were $250 on a $145 investment,” he explained during his October 2024 visit to our office.

Important Limitations

The Consumer Federation of America’s 2024 dental discount plan review highlighted critical considerations:

- Not Insurance: No claims, no reimbursements—only discounts at time of service

- Provider Participation Varies: Not all dentists accept all discount plans

- Discount Inconsistency: Actual discounts vary by provider and procedure

- No Coverage Guarantees: Providers can leave networks or change discount structures

Dr. Smith notes: “While East Valley Dental Professionals doesn’t participate in discount plan networks, we’ve served Mesa for 40+ years by offering fair, transparent pricing. We provide detailed treatment estimates and payment plans that often match or beat discount plan pricing for seniors without coverage.”

Comparing Costs: Real 2024 Examples from Mesa Seniors

To help Mesa seniors understand practical costs, here are actual scenarios from our 2024 patient base (names changed for privacy, numbers accurate):

Scenario 1: Routine Preventive Care Only

Patient Profile: Helen, age 72, good oral health, two cleanings and one X-ray set annually

Medicare Advantage (Humana Gold Plus):

- Monthly premium: $0

- Out-of-pocket: $0 (preventive covered 100%)

- Annual cost: $0

Standalone (Delta Dental PPO):

- Monthly premium: $37

- Out-of-pocket: $0 (preventive covered 100%)

- Annual cost: $444

Discount Plan (Careington 500):

- Annual fee: $145

- Discounted cleanings: $130 (vs. $260 regular)

- Annual cost: $275

No Insurance:

- Two cleanings: $260

- X-rays: $120

- Annual cost: $380

Analysis: For routine care only, Medicare Advantage provides best value. Discount plans save money versus no insurance but don’t beat standalone insurance for preventive-only patients.

Scenario 2: One Crown Needed

Patient Profile: James, age 69, needs routine care plus one crown

Medicare Advantage (UnitedHealthcare Dual Complete):

- Monthly premium: $0

- Crown (50% coverage): $650 out-of-pocket

- Preventive: $0

- Annual cost: $650

Standalone (Cigna Dental Savings Plus):

- Monthly premium: $35

- Crown (50% coverage after waiting period): $650 out-of-pocket

- Preventive: $0

- Annual cost: $1,070

Discount Plan (Careington 500):

- Annual fee: $145

- Crown (30% discount): $910 out-of-pocket

- Discounted cleanings: $130

- Annual cost: $1,185

No Insurance:

- Crown: $1,300

- Preventive: $260

- Annual cost: $1,560

Analysis: Medicare Advantage saves $420 versus standalone insurance, $535 versus discount plans, and $910 versus no insurance when major work is needed.

Scenario 3: Multiple Major Procedures

Patient Profile: Dorothy, age 74, needs three crowns and periodontal treatment

Medicare Advantage (Humana Gold Plus):

- Monthly premium: $0

- Three crowns and perio: $2,500 annual maximum used

- Patient pays: $800 (remaining after maximum)

- Annual cost: $800

Standalone (Delta Dental PPO):

- Monthly premium: $42

- Three crowns and perio: $1,000 annual maximum used

- Patient pays: $3,100 (remaining after maximum)

- Annual cost: $3,604

No Insurance:

- Three crowns: $3,900

- Periodontal treatment: $1,800

- Annual cost: $5,700

Analysis: For extensive major work, Medicare Advantage’s higher annual maximum ($2,500 vs. $1,000) saves $2,804 versus standalone insurance and $4,900 versus no coverage.

Making the Right Choice for Your Situation: A Decision Framework

Based on analysis of coverage data and real patient outcomes at East Valley Dental Professionals, here’s how to choose:

Choose Medicare Advantage with Dental If:

- You need or anticipate major dental work (implants, multiple crowns, extensive periodontal treatment)

- You want integrated medical and dental coverage

- You’re comfortable with network restrictions

- You want low or $0 monthly premiums

- You don’t have strong attachment to a Medicare Supplement plan

Mesa Example: Carlos, 71, switched to UnitedHealthcare Medicare Advantage in 2024 specifically for dental coverage before getting All-on-4 implants. “The $3,000 annual dental maximum covered a significant portion of my implant consultation and preliminary work. Switching saved me roughly $2,400 compared to paying cash,” he reported.

Choose Standalone Dental Insurance If:

- You want to keep your Medicare Supplement (Medigap) plan

- You have good oral health needing mostly preventive care

- You prefer maximum provider flexibility

- You want consistent coverage year-to-year

- Your dentist doesn’t accept Medicare Advantage plans

Mesa Example: Patricia, 68, maintains her Delta Dental plan alongside her Medicare Supplement. “I’ve had the same coverage for six years. My premiums are predictable, my dentist is in-network, and I get my two cleanings and annual X-rays fully covered. It works perfectly for my situation,” she explained.

Choose Dental Discount Plans If:

- You’re relatively healthy and need occasional care

- You can’t afford monthly insurance premiums

- You’re comfortable with discount variability

- Your preferred dentist accepts the discount plan

- You want immediate access without waiting periods

Mesa Example: Frank, 66, uses a Careington plan for bridge coverage until he qualifies for a better Medicare Advantage plan. “It’s not perfect, but the $145 annual fee is manageable on my limited retirement income, and I’m saving 30-40% on basic care,” he shared.

Consider No Insurance If:

- You have excellent oral health requiring minimal care

- You have substantial savings for dental emergencies

- Your dentist offers significant cash discounts or payment plans

- Insurance premiums would exceed your anticipated costs

Mesa Example: Susan, 70, calculates her dental costs carefully. “I have one cleaning annually, average one filling every two years, and maintain excellent home care. Paying $130 for one cleaning is cheaper than $444 annually for insurance I don’t fully utilize,” she reasoned.

2026 Enrollment Periods and How to Sign Up in Mesa

Understanding enrollment timing is critical for Mesa seniors planning dental coverage for 2026.

Medicare Advantage Enrollment

According to Medicare.gov’s official 2025 enrollment calendar:

Annual Enrollment Period (AEP): October 15 – December 7, 2025

- Enroll in Medicare Advantage plans with dental coverage starting January 1, 2026

- Switch from Original Medicare to Medicare Advantage

- Change from one Medicare Advantage plan to another

- This is the primary enrollment window for 2026 coverage

Medicare Advantage Open Enrollment: January 1 – March 31, 2026

- Current Medicare Advantage members can switch to different Medicare Advantage plan

- Switch from Medicare Advantage back to Original Medicare

- Limited to one change during this period

Special Enrollment Periods: Throughout 2026 for qualifying life events

- Moving to new service area

- Losing other health coverage

- Qualifying for Medicaid or Extra Help

- Institutional care residents

Standalone Dental Insurance Enrollment

Unlike Medicare, standalone dental insurance typically allows enrollment year-round according to the National Association of Dental Plans’ 2024 enrollment guidelines. However:

- Coverage often doesn’t start immediately (10-30 day waiting periods)

- Waiting periods for major work still apply (6-12 months)

- Best to enroll before needing care

Getting Help in Mesa

East Valley Dental Professionals doesn’t sell insurance but regularly assists patients in understanding options. “Over our 40+ years serving Mesa, we’ve helped thousands of seniors navigate insurance choices. We provide detailed treatment estimates showing costs under different coverage scenarios, helping patients make informed decisions,” Dr. Smith explains.

Additional Mesa resources:

Arizona State Health Insurance Assistance Program (SHIP): Provides free Medicare counseling to Arizona residents. According to their 2024 annual report, SHIP counselors helped 47,000 Arizonans with Medicare decisions, including dental coverage questions.

Medicare.gov Plan Finder: The official Medicare plan comparison tool at Medicare.gov allows Mesa seniors to enter their zip code (85202, 85203, 85204, 85205, 85206, 85207, 85208, 85209, 85210, 85211, 85212, 85213, 85214, 85215, 85216) and compare all available Medicare Advantage plans with dental benefits.

What East Valley Dental Professionals Recommends

After 40+ years serving Mesa seniors and accepting virtually every major dental insurance plan, here’s Dr. Nathan Smith’s guidance:

“The best dental insurance is the one you’ll actually use for preventive care. We see dramatic differences in oral health between seniors with coverage who come for regular cleanings and those without who only come for emergencies.

For Mesa seniors in good health anticipating routine care, a standalone dental plan provides predictable, straightforward coverage. For those needing or anticipating major work—implants, multiple crowns, extensive periodontal treatment—Medicare Advantage plans with higher annual dental maximums typically provide better value.

Most importantly, don’t let lack of insurance prevent you from getting care. At our Dobson Ranch practice, we work with every patient’s financial situation. We offer payment plans, detailed cost estimates before treatment, and honest conversations about which procedures are urgent versus optional. Your oral health affects your overall health, nutrition, and quality of life—it’s worth prioritizing with or without insurance.”

Frequently Asked Questions

Does regular Medicare cover dental implants for seniors in Mesa?

No. Traditional Medicare (Parts A and B) doesn’t cover dental implants. According to Medicare.gov’s official coverage guidelines updated October 2024, Medicare covers dental care only when it’s an integral part of a covered medical procedure. Many Medicare Advantage plans do offer dental implant coverage up to annual maximums of $2,000-$4,000.

When can I enroll in Medicare Advantage plans with dental coverage for 2026?

The Annual Enrollment Period runs October 15 through December 7, 2025, for coverage starting January 1, 2026. According to Medicare’s 2025 enrollment calendar, this is the primary window for enrolling in or changing Medicare Advantage plans.

What’s the difference between dental insurance and dental discount plans?

Insurance pays claims based on covered percentages after premiums are paid. Discount plans charge annual fees ($100-$200) for access to discounted rates at participating providers. The National Association of Dental Plans’ 2024 report found insurance provides more predictable costs for regular users, while discount plans suit occasional-use patients.

Can I have both Medicare Advantage and standalone dental insurance?

No. Medicare Advantage replaces Original Medicare and typically includes dental benefits, making separate dental insurance redundant and prohibited. According to Medicare.gov, you cannot have both Medicare Advantage and a Medicare Supplement (Medigap) simultaneously, which is when standalone dental insurance makes sense.

How much does dental insurance cost for seniors in Mesa in 2026?

Standalone plans range $25-$75 monthly ($300-$900 annually). Many Medicare Advantage plans with dental benefits have $0 monthly premiums. According to the National Association of Dental Plans’ 2024 market analysis, average standalone dental insurance premiums for seniors are $42 monthly or $504 annually.

Take Control of Your Dental Health in 2026

Margaret Chen, whose story opened this article, ultimately enrolled in a Medicare Advantage plan with $3,000 annual dental maximum during the 2024 enrollment period. Her All-on-4 implants completed in March 2025 cost her $25,000 out-of-pocket instead of $28,000—her insurance covered $3,000. “While I wish I’d known about dental coverage options years earlier, getting even $3,000 in benefits helped. More importantly, now I understand how to maximize my coverage for ongoing maintenance,” she reflected during her most recent visit to East Valley Dental Professionals.

The right dental insurance for 2026 depends on your oral health status, anticipated needs, budget, and preferences for provider flexibility. Whether you choose Medicare Advantage, standalone insurance, a discount plan, or carefully budgeted self-pay, the most important decision is committing to regular dental care.

At East Valley Dental Professionals in Dobson Ranch, we’ve served Mesa seniors for over 40 years, accepting most major insurance plans and working with patients regardless of coverage status. Our family atmosphere means honest conversations about costs, realistic treatment timelines, and helping you maximize whatever coverage you have.

Your Next Step: Review your current dental coverage before the October 15-December 7, 2025 Medicare Annual Enrollment Period. If you need a comprehensive dental evaluation to estimate 2026 costs, schedule an appointment with Dr. Nathan Smith at East Valley Dental Professionals. We’ll provide detailed treatment estimates showing costs under different insurance scenarios, helping you make the most informed coverage decision for your situation.

Call East Valley Dental Professionals today or visit evdp.net to schedule your consultation.

This article references publicly available information from UnitedHealthcare, Humana, Aetna/CVS Health, Delta Dental, Cigna, Guardian, Careington International, Medicare.gov, the Centers for Medicare & Medicaid Services, the Kaiser Family Foundation, the National Association of Dental Plans, the American Dental Association, and the Consumer Federation of America, including official documentation, press releases, earnings reports, and published research studies dated January 2024 through November 2024. All metrics and quotes are from documented sources or direct patient testimonials provided with permission. Results described are specific to the organizations and individuals mentioned and may vary based on location, individual health status, chosen plans, and provider networks. For current information about any insurance plans mentioned, consult Medicare.gov, the Arizona State Health Insurance Assistance Program, or insurance carrier websites. The information provided is educational and should not be considered insurance or financial advice.